In this segment, we justify some of the property is that the correlation coefficient that we claimed a little earlier.

The most important properties of the correlation coefficient lies between minus 1 and plus 1.

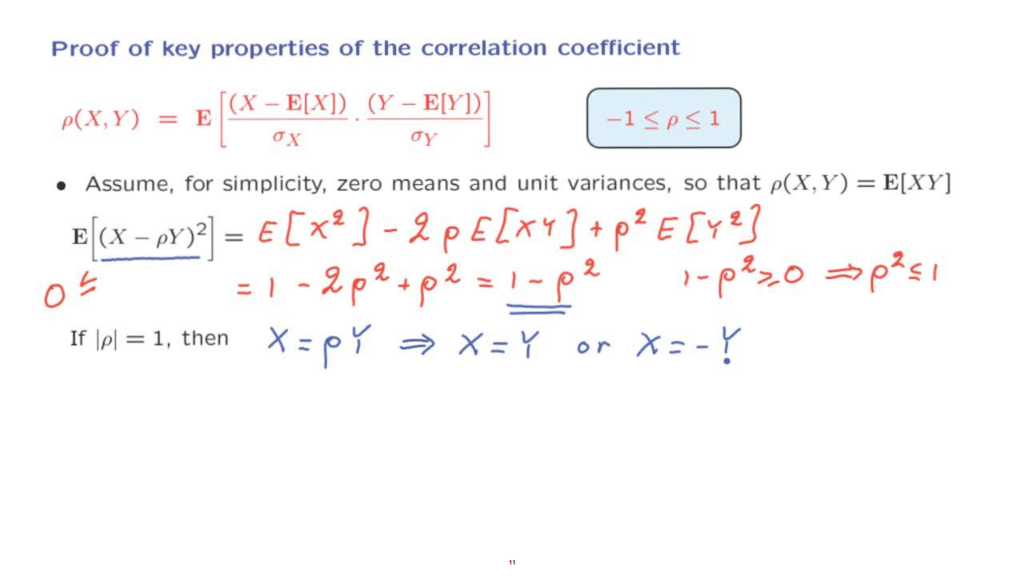

We will prove this property for the special case where we have random variables with zero means and unit variances.

So standard deviations are also 1, so most of the terms here disappear and the correlation coefficient is simply the expected value of X times Y.

We will show that in this special case the expected value of X times Y lies between minus 1 and 1.

But the proof of this fact remains valid with a little bit of more algebra along similar lines for the general case.

What we will do is we will consider this quantity here and expand this quadratic and write it as expected value of X squared.

Then there’s a cross term, which is minus 2 rho, the expected value of X times Y, plus rho squared, expected value of Y squared.

Now since we assume that the random variables have 0 mean, this is the same as the variance and we assume that the variance is 1, so this term here is equal to 1.

Now, the expected value of X times Y is the same as the correlation coefficient in this case.

So we have minus 2 rho squared and from here we have rho squared.

And by the previous argument, again this quantity, according to our assumptions, is equal to 1 so we’re left with this expression, which is 1 minus rho squared.

Now, notice that this is the expectation of a non-negative random variable so this quantity here must be non-negative.

Therefore, 1 minus rho squared is non-negative, which means that rho squared is less than or equal to 1.

And that’s the same as requiring that rho lie between minus 1 and plus 1.

And so we have established this important property, at least for the special case of 0 means and unit variances.

But as I mentioned, it remains valid more generally.

Now let us look at an extreme case, when the absolute value of rho is equal to 1.

What happens in this case?

In that case, this term is 0 and this implies that the expected value of the square of this random variable is equal to 0.

Now here we have a non-negative random variable, and its expected value is 0, which means that when we calculate the expected value of this there will be no positive contributions and so the only contributions must be equal to 0.

This means that X minus rho Y has to be equal to 0 with probability 1.

So X is going to be equal to rho times Y and this will happen with essential certainty.

Now also because the absolute value overall is equal to 1, this means that we have either X equal to Y or X equals to minus Y, in case rho is equal to minus 1.

So we see that if the correlation coefficient has an absolute value of 1, then X and Y are related to each other according to a simple linear relation, and it’s an extreme form of dependence between the two random variables.