We now study a model that involves the sum of independent random variables, but with a twist.

It’s going to be the sum of a random number of independent random variables, as opposed to a fixed number.

This is a model that shows up in a variety of applications, but it will also help us fine tune our command of the law of iterated expectations, and the law of total variance.

The story goes as follows– you go shopping and you visit a number of stores, except that the number of stores that you will visit, is itself a random variable.

At each one of the stores, you spend a certain amount of money.

We denote it by Xi.

And we make the assumption that the Xi’s are drawn from a certain distribution.

They’re identically distributed.

And they’re independent of each other.

We also make the assumption that the Xi’s are independent of capital N.

This means that no matter how many stores you visit, the Xi, the amount of money you spend in each one of the stores that you visit, is a random variable that’s drawn from a common distribution, which does not change, no matter what capital N is.

With these assumptions in place, let us now focus on the total amount of money that you’re spending.

This is the sum of random variables, but with the extra twist that the index goes up to capital N, which is itself a random variable.

How do we deal with this situation?

One approach that’s always worth trying when faced with a complicated problem is to try to condition on some information that will make the problem easier.

In this case, we can condition on the value of capital N taking a fixed specific value because in that case, we will be dealing with the sum of a finite number of random variables where that number is a fixed, specific number.

And this is a situation we have encountered before and know how to deal with it.

So let us get started.

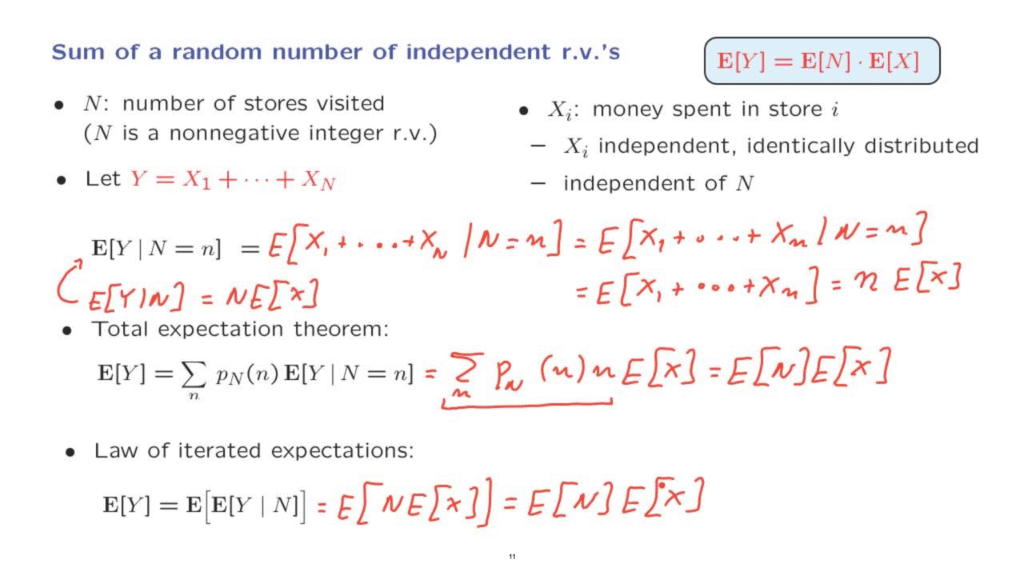

Let us calculate the expected value of Y, if we condition on the number of stores.

Let’s say, for example, someone tells us that we visited five stores.

Then, the expected value of Y is going to be the expected value of the sum of the amount of money you spent in each one of those five stores.

In our instance, it’s that random variable, capital N.

But since I told you that capital N takes a specific numerical value, this means that this instance of capital N, in the index of the summation, can be replaced by little n.

If I tell you that capital N is equal to little n, then this number here, capital N, becomes the same as little n.

Here we use now the assumption that capital N is independent from the Xi’s.

Here we have the sum of a fixed number of random variables.

All of them are independent of capital N.

If I give you some information on capital N, this does not change the distribution of the Xi’s, so the conditioning does not affect the answer.

The conditional expectation is going to be the same as the unconditional expectation.

And now we have the expected value of a sum of random variables.

Each one of them has a common expectation that’s denoted with this notation.

This is the common expected value of all the Xi’s, and we’re adding n of them, so we obtain n times this expectation.

Now let us apply the total expectation theorem.

We take the familiar form of the total expectation theorem, and in here, ‘ we can plug in the expression that we have just found, which is n times expected value of X.

Now the expected value of X is just a number.

And then we have this summation here, which we recognize to be just the definition of the expected value of N.

And so we come to the conclusion that the expected amount of money that you will be spending is equal to the following product– the expected number of stores that you visit times the expected amount of money that you will be spending in each store.

This is a quite plausible answer.

It makes sense.

On the average, the amount of money you spend is equal to the average number of stores times the average amount of money in each store.

So it is intuitively what you might expect.

On the other hand, we know that reasoning “on the average” does not always give us the right answers.

So it’s important to corroborate this particular formula by working out a mathematical derivation.

Now let us carry out a second mathematical derivation using the law of iterated expectations.

To use the law of iterated expectations, we need to put our hands on this random variable– the abstract conditional expectation.

What is this object?

It’s a random variable that takes this value whenever capital N is equal to little n.

So it’s an object that takes this value whenever capital N is equal to little n.

But that object is the same as this random variable because this is the random variable that takes the value here when capital N is equal to little n.

Therefore, the abstract conditional expectation takes this particular form here, which we can substitute inside this expectation here.

And now notice that the expected value of X is a constant, so it can be pulled outside this expectation.

And we’re left with a product of the expected value of N times the expected value of X.

So this completes the derivation of the expected value of the sum of a random number of random variables.